There are two popular types of term life policies: Yearly Renewable Term and Level Term. The main difference between the two types is the duration of the policy and how the premiums are charged:

Yearly Renewable Term Policy

Under a Yearly Renewable Term policy, your policy will be renewed year-to-year. Your premium starts low, but as you renew, it will increase slightly every year as you grow older.

Level Term Policy

Under a Level Term policy, as long as your premium payments are up to date, your policy will be in force for the whole “term” of the policy. At Fi Life, you can choose a level term duration of 10, 15, 20, 25 or 30 years. This means that your premiums will be fixed or “level” for duration.

Which is more suitable?

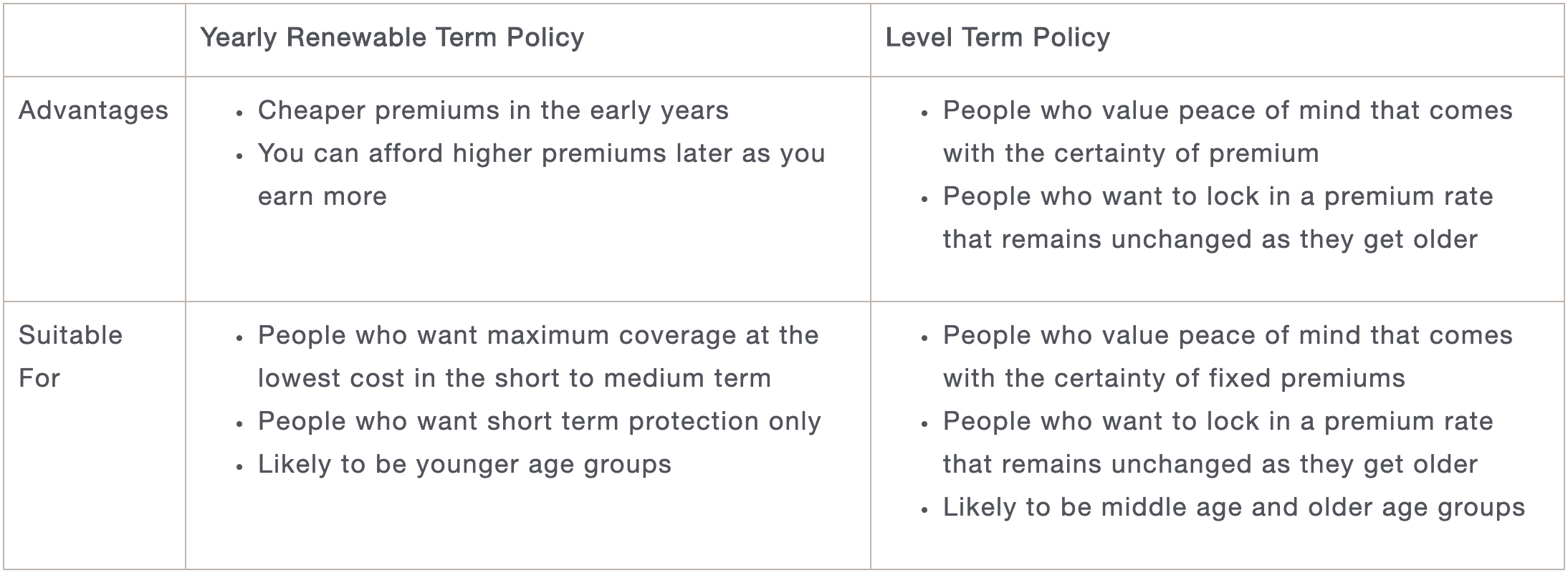

This depends on your personal preference and circumstances. If you would like to pay less at the beginning but renew at a slightly higher rate as your income increases each year, then a Yearly Renewable Term policy would be suitable. You might also choose a Yearly Renewable Term policy for short term protection, say for example, if your children are entering the workforce soon, and you just need a few more years of protection until they become fully independent.

However, if you prefer to have the security of knowing that your premiums will be fixed for the next 10 to 30 years, then the Level Term policy would be more suitable.

You can get a quote from us, and then compare the future premium schedule of a Yearly Renewal Term policy versus the fixed premium schedule of a Level Term policy.

Example

Let’s take an example of a female Non-Smoker, age 39.

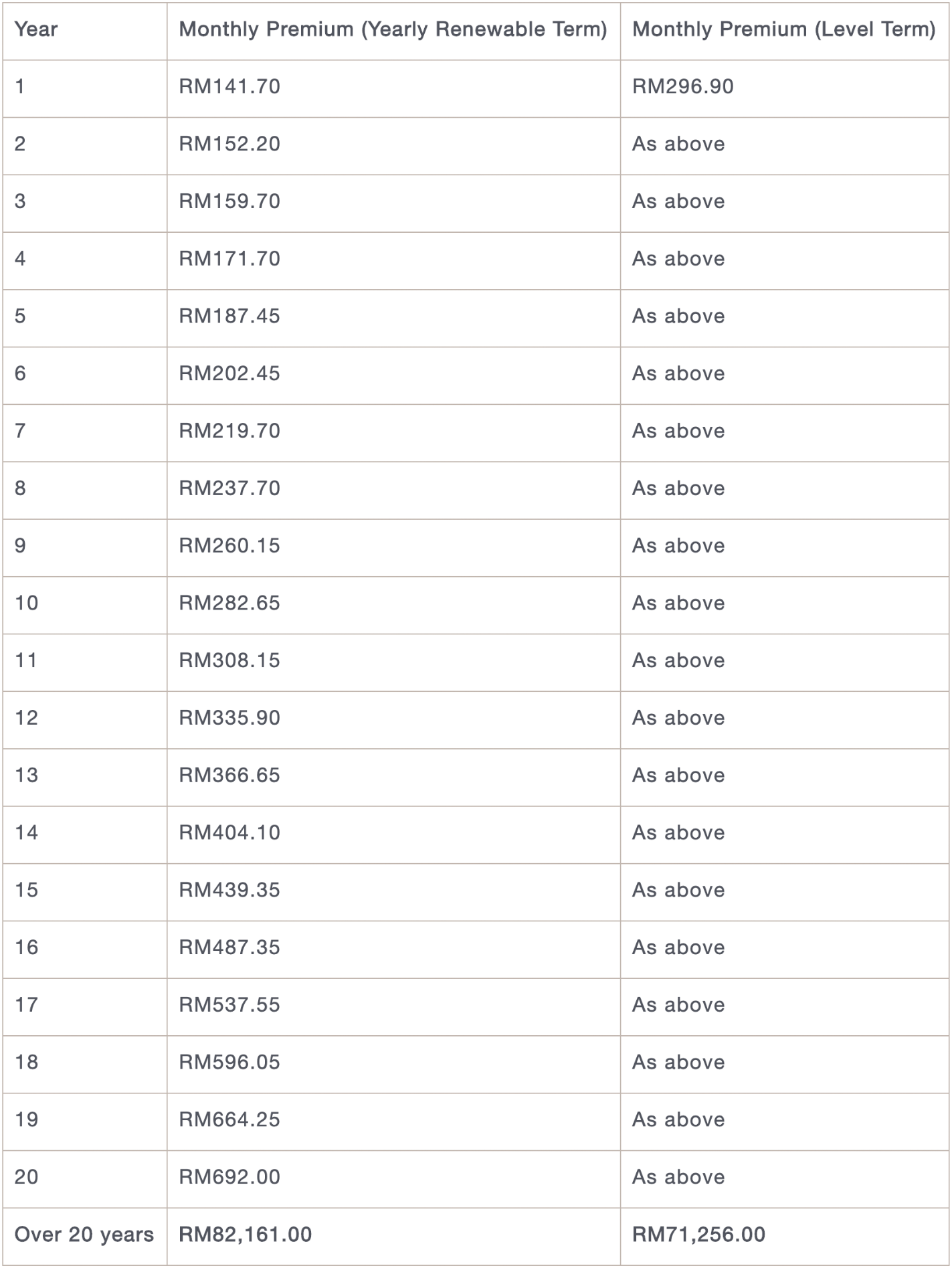

Here’s the premium difference between a Yearly Renewable Term policy and say Level Term policy for a duration of 20 years, for RM1 million sum assured:

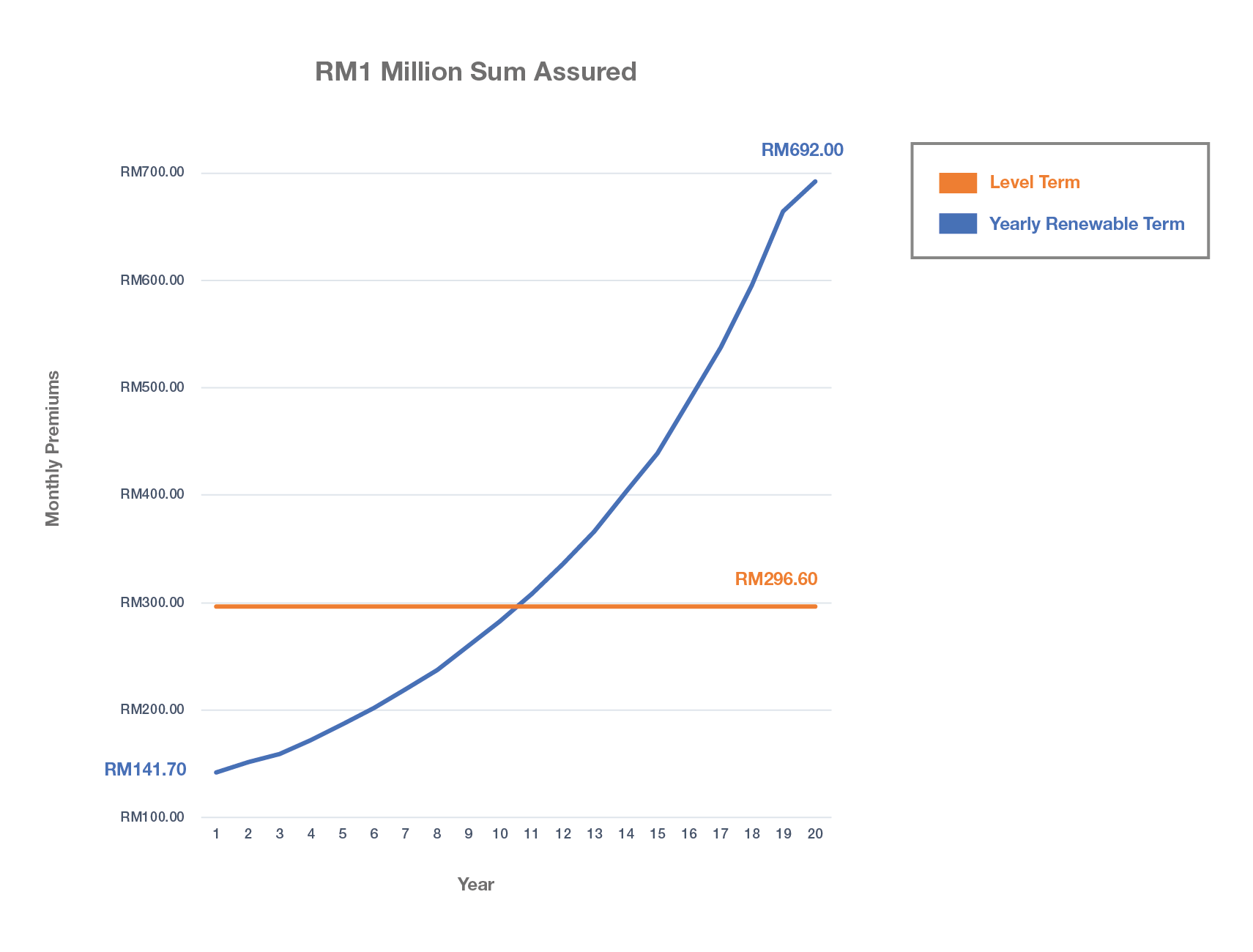

The premium table above is expressed graphically in the chart above showing the Yearly Renewable Term premiums, which increases over time, and the Level Term premiums, which is fixed and is expressed as a straight line. While the premium for the Level Term policy remains fixed at RM296.90 per month for 20 years, the premium for the Yearly Renewable Term policy starts at 53% cheaper at RM141.70 per month. However, the premium for the Yearly Renewable Term policy becomes more expensive than the Level Term policy after year 11. By year 20, the premium for the Yearly Renewable Term policy is RM692.00 per month, about 2.3 times more than the premium for the Level Term policy. Over the course of the 20 years, the premiums for the Yearly Renewable Term policy will amount to RM82,161 compared to RM71,256 for the Level Term policy.

Which policy is better for the woman in this example really depends on her preference. Just because she pays, over 20 years, RM10,000 more for a Yearly Renewable Policy does not necessarily mean that the level term policy is more suitable for her. In the first 10 years, when the premiums of the Yearly Renewable Term policy were cheaper than that of the Level Term policy, she might have used the cost savings to invest in unit trusts, equities or other investments, that might have returned to her more than the RM10,000 difference in the cost of the two policies over 20 years.

For those of you who want to know the precise monthly premiums for the Yearly Renewable Term policy for this example, please see the premium table below.