How Much Life Insurance Do You Need?

Simply put, it’s the amount of money your family needs to get by in if you’re not around. Here’s how to work this out:

- 1a. How much money would your family need each month to maintain their current standard of living?

Have a look at your bank and credit card statements to work out how much you spend as a family on a monthly basis. For now, do not include repayments for your home mortgage or car loans. Multiply your monthly expenditure by 12, and that’s your family’s annual expenditure.

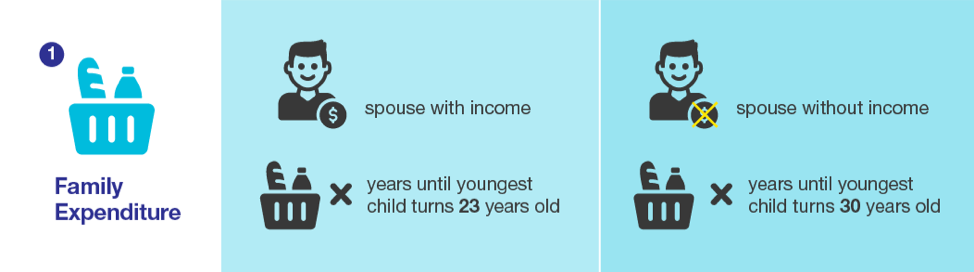

- 1b. Is your surviving spouse working and earning an income?

If so, is his/her annual take-home pay enough to cover your annual family expenditure above? If not, make a note of the shortfall on an annual basis.*

- 1c. Estimate how many years your family will need to fund the annual shortfall.

If your spouse is working, you really need to fund the shortfall until your youngest child is of working age (say 23 years old) and can support herself. If your spouse is not working, you will need to fund the shortfall until your children are able to support your spouse financially (say when the eldest turns 30 years old, an additional 7 years from the previous example).

- 2. Do you have any big loan obligations e.g. mortgage or car loans?

Total up all your loans, this will be the amount your estate will need to repay if you want to remove the burden of the repayment of loans from your family if something should happen to you.

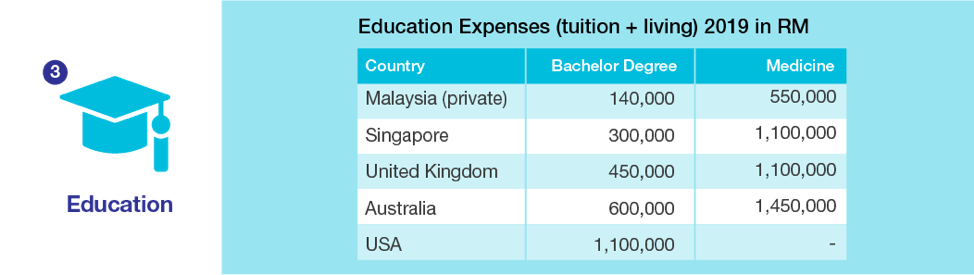

- 3. Do you have school-going children?

If so, calculate how much their education will cost. The chart above is a guide to Malaysian private university as well as overseas education cost. You will also need to add primary and secondary school education costs too if your children are attending private school.

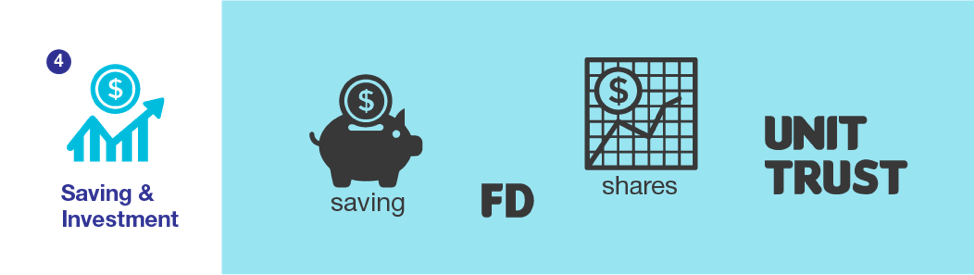

- 4. Do you have any savings or assets that can help defray some of your liabilities e.g. fixed deposit, unit trusts, shares, or a fully paid up investment property, EPF funds?

Don’t include the family home as part of your assets, your family will still need to live there.

Once you have the above numbers, use our calculator to find out how much life insurance you need.

Example: Joyce, working mother

Joyce, aged 35, is a working mother, with 2 children, aged 6 and 8. Her family household expenses excluding mortgage and car loan repayments amount to RM10,000 per month. Her husband’s take-home pay (after deducting EPF and PCB) is about RM8,000 per month, whilst hers is RM9,000 per month. There’s still about RM500,000 left on her mortgage, and RM70,000 on her car loan.

There are no big important expenditures foreseeable in the future, but she is likely to send her children to a private secondary school in 4 and 6 years time, with fees about RM25,000 per academic year per child for 6 years (total of RM300,000 for her 2 children), and, a local private university education for her 2 children (total of RM280,000 for her 2 children). She has savings of about RM30,000, and unit trusts that are valued at RM70,000. She has about RM80,000 in her EPF account.

| Joyce’s future Financial Needs versus (Assets/income) | Total | |

| 1. |

a. Family living expenses

b. Husband’s salary to defray living expenses

Shortfall to cover in living expenses

|

RM330,000 |

| 2. |

Outstanding liability

|

RM570,000 |

| 3. |

Children’s education

|

RM840,000 |

| 4. |

Savings and investment

|

RM180,000 |

|

Total life insurance needed

|

RM1,560,000 |

This looks a lot, but Fi offers up to RM1 million in life insurance coverage. In Joyce’s case, if she’s a non-smoker and has no prior medical problems, her premiums will be around RM116.25 per month.

Use our life insurance calculator to see how much life cover you need. And then get a quote from Fi Life!